Key Takeaways:

- Company liquidation in Dubai is the formal process of closing a business, settling debts, selling assets, and de-registering the entity.

- Liquidation can be voluntary (initiated by owners) or compulsory (court-ordered due to insolvency).

- Appointing a licensed liquidator (typically an audit firm) is a mandatory step for most liquidations.

- All liabilities, including employee dues, supplier payments, and government fines, must be settled before final de-registration.

- The process for liquidating a Business setup in Dubai varies slightly between mainland and free zone companies, but both require strict adherence to legal procedures.

While the aspiration for every Business setup in Dubai is sustained growth and success, circumstances can arise where winding down operations becomes necessary. This process, known as liquidation, is a formal and legally mandated procedure to close a company. It involves selling off assets, settling all outstanding liabilities, and formally de-registering the business with the relevant authorities. Whether due to strategic decisions, financial difficulties, or a change in business focus, understanding the liquidation process is crucial for any entrepreneur operating in Dubai to ensure a compliant and penalty-free exit.

Why a Structured Liquidation is Vital for Business setup in Dubai?

Initiating a structured liquidation for your Business setup in Dubai is not merely a formality; it’s a critical legal and financial necessity that protects stakeholders and ensures compliance. Skipping or mishandling the liquidation process can lead to severe repercussions.

- Avoiding Legal Penalties and Fines:

- Simply abandoning a company or letting its license expire without formal liquidation can result in substantial fines from the Department of Economy and Tourism (DET) for mainland companies or free zone authorities. These fines can accumulate, potentially leading to a permanent ban on the owners or partners from undertaking future Business setup in Dubai.

- Authorities closely monitor active licenses. If a company remains registered but is non-operational or has outstanding obligations, it is considered non-compliant.

- Protecting Shareholders and Directors from Liabilities:

- Until a company is officially de-registered, its shareholders and directors can remain legally liable for its outstanding debts and obligations. A proper liquidation process ensures all liabilities are settled, providing a clean break for the owners.

- This separation of personal and corporate liability is a cornerstone of the limited liability company (LLC) structure, but it only holds true if the company is dissolved according to the law.

- Ensuring Fair Treatment of Creditors:

- A structured liquidation process mandates that the company’s assets are liquidated and the proceeds distributed among creditors in a legally defined order of priority. This ensures fairness and transparency, minimizing disputes and potential lawsuits from unsatisfied creditors.

- This includes banks, suppliers, landlords, and other service providers.

- Managing Employee Obligations:

- A key aspect of liquidation involves settling all employee end-of-service benefits (gratuity), outstanding salaries, and any other dues as per UAE Labour Law. All employee visas sponsored by the company must also be cancelled in accordance with immigration regulations.

- Failing to address employee entitlements can lead to labor complaints, travel bans, and significant fines, affecting the ability of owners and partners to engage in future business activities in the UAE.

- Maintaining Business Reputation and Future Prospects:

- A clean exit demonstrates professionalism and adherence to legal processes. This is vital for maintaining a good business reputation in the UAE.

- For owners or partners who wish to conduct future Business setup in Dubai, a history of a properly liquidated company is viewed favorably, whereas a record of non-compliance can create significant hurdles.

By undertaking a formal liquidation process for your Business setup in Dubai, you not only fulfill your legal obligations but also safeguard your personal and financial well-being while preserving your standing in the business community.

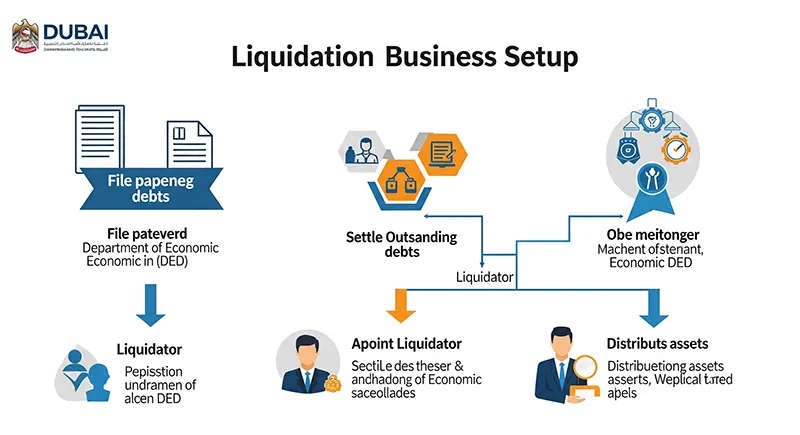

Role of a Liquidator in Business setup in Dubai Liquidation

A crucial and often mandatory component of the liquidation process for a Business setup in Dubai is the appointment of a licensed liquidator. The liquidator plays a central and legally defined role in ensuring the winding-up process is conducted compliantly and efficiently.

- Mandatory Appointment:

- For most company structures in Dubai, particularly Limited Liability Companies (LLCs) on the mainland and many free zone entities, appointing a licensed liquidator (typically a registered audit firm) is a legal requirement. This is stipulated by UAE Commercial Companies Law and respective free zone regulations.

- The liquidator must be approved by the Department of Economy and Tourism (DET) for mainland companies or the specific free zone authority (e.g., SPC Free Zone in Dubai authority).

- Acceptance and Initial Formalities:

- Once appointed by a shareholder resolution, the liquidator provides a formal acceptance letter to the relevant licensing authority, confirming their role and responsibility for the liquidation process.

- This acceptance letter, along with the shareholder resolution, initiates the official liquidation process.

- Taking Control of Company Assets and Records:

- The liquidator assumes control over the company’s assets, books of accounts, and financial records. They are responsible for creating a comprehensive inventory of all assets and liabilities.

- This includes physical assets, bank accounts, receivables, and any outstanding payables.

- Notification to Creditors and Public Advertisement:

- A key duty of the liquidator is to formally notify all known creditors of the company’s liquidation. For mainland LLCs, this also involves publishing a public notice of liquidation in two local newspapers (one typically in Arabic), providing a specific grace period (usually 45 days) for creditors to submit any claims.

- This ensures transparency and allows all parties with financial interests to come forward.

- Asset Realization and Debt Settlement:

- The liquidator’s primary financial responsibility is to sell or realize the company’s assets to generate funds. These funds are then used to settle all outstanding liabilities in a legally prescribed order of priority.

- This hierarchy generally prioritizes secured creditors (like banks), followed by employees (for end-of-service benefits and salaries), then unsecured creditors (suppliers, landlords), and finally, shareholders (if any surplus remains).

- Obtaining Clearance Certificates:

- The liquidator is instrumental in obtaining necessary No Objection Certificates (NOCs) from various government departments and utility providers, confirming that the company has no outstanding dues or obligations. This typically includes:

- Dubai Electricity and Water Authority (DEWA)

- Telecom providers (Etisalat/Du)

- Ministry of Human Resources & Emiratisation (MOHRE) for labor clearances

- General Directorate of Residency and Foreigners Affairs (GDRFA) for immigration clearances and visa cancellations

- Federal Tax Authority (FTA) for VAT and Corporate Tax deregistration.

- Customs (if applicable).

- They also ensure the closure of the company’s bank accounts and obtain closure letters.

- The liquidator is instrumental in obtaining necessary No Objection Certificates (NOCs) from various government departments and utility providers, confirming that the company has no outstanding dues or obligations. This typically includes:

- Preparation of Final Liquidation Report:

- At the conclusion of the process, the liquidator prepares a comprehensive Final Liquidation Report (or Statement of Affairs). This report details all assets realized, debts settled, and confirms that all legal procedures have been followed. It also states that there are no pending claims against the company.

- Submission for De-registration:

- The liquidator submits the final report along with all clearance certificates and supporting documentation to the relevant licensing authority (DET or free zone authority) for final approval and company de-registration.

By entrusting the liquidation to an experienced and approved professional, businesses undergoing a Business setup in Dubai closure can navigate the complexities efficiently and ensure full compliance.

Liquidating Business setup in Dubai: Mainland Process

Liquidating a mainland Business setup in Dubai (typically an LLC) is a multi-stage process governed by the Department of Economy and Tourism (DET) and other relevant authorities. It generally involves two key phases: initial approval and final cancellation.

Phase 1: Initial Approval for Liquidation

- Shareholder Resolution:

- The process begins with the shareholders or partners formally passing a resolution to liquidate the company. This resolution must be printed on the company letterhead, signed by all authorized parties, and notarized by a Public Notary in Dubai. This document explicitly states the decision to liquidate and appoints a licensed liquidator. For Sole Establishments, the owner simply notifies DET of the intent to close.

- Appoint a Licensed Liquidator:

- Engage a licensed audit firm or approved liquidator. The liquidator will provide an official acceptance letter, on their letterhead, confirming their appointment and willingness to undertake the liquidation. This letter must include their license details.

- Submit Initial Documents to DET:

- Submit the notarized Shareholder Resolution and the Liquidator’s Acceptance Letter, along with a copy of the valid trade license, passport copies, and Emirates IDs of all shareholders, to the DET.

- DET will review these documents and issue an initial approval, allowing the liquidation process to officially commence.

- Publish Newspaper Advertisement (Mandatory for LLCs):

- Within two working days of receiving initial approval, the appointed liquidator must publish a notice of the company’s liquidation in two local Arabic newspapers.

- This advertisement serves as a public notification to creditors, allowing them a 45-day grace period from the date of publication to submit any claims against the company. This step is crucial for legal compliance and protecting third-party rights.

Phase 2: Final Cancellation

- Clearance of All Liabilities and Obtaining NOCs:

- This is the most time-consuming phase. During and after the 45-day notice period, the liquidator will work to settle all company liabilities and obtain clearance letters (No Objection Certificates – NOCs) from various government entities and service providers:

- Employee Dues: Settle all end-of-service benefits, final salaries, and cancel all employee and investor visas. Obtain clearance from the Ministry of Human Resources & Emiratisation (MOHRE) and the General Directorate of Residency and Foreigners Affairs (GDRFA).

- Utility Providers: Obtain NOCs from Dubai Electricity and Water Authority (DEWA) and telecom providers (Etisalat/Du).

- Landlord: Ensure the tenancy contract is terminated and all payments are settled. Cancel the Ejari certificate.

- Bank: Close all corporate bank accounts and obtain bank account closure letters.

- Federal Tax Authority (FTA): Apply for VAT deregistration (if applicable) and ensure all tax obligations (including Corporate Tax) are met. Obtain an FTA clearance.

- Dubai Customs: If applicable for trading companies.

- Other Regulatory Bodies: If the business activity was regulated (e.g., healthcare, education), obtain specific NOCs from relevant authorities.

- Fines/Penalties: Clear any outstanding fines or penalties with DET or other departments.

- This is the most time-consuming phase. During and after the 45-day notice period, the liquidator will work to settle all company liabilities and obtain clearance letters (No Objection Certificates – NOCs) from various government entities and service providers:

- Final Liquidation Report:

- Once all liabilities are settled and all necessary clearances are obtained, the liquidator prepares the Final Liquidation Report (Statement of Affairs). This report confirms that all assets have been accounted for, debts paid, and that there are no pending claims.

- Submit Final Documents to DET:

- Submit the Final Liquidation Report, original newspaper advertisement proofs, all original clearance certificates, and the completed final de-registration application form to DET.

- Pay Final Fees and Receive De-registration Certificate:

- DET will review the final submission. Upon approval and payment of any final de-registration fees, DET will issue the official Trade License Cancellation Certificate, formally dissolving the company.

The entire process for mainland LLC liquidation typically takes 60-90 days, but this can vary based on the complexity of the company’s affairs, the number of employees, and the speed of obtaining clearances. Engaging a business setup specialist and an approved liquidator is highly recommended to streamline this intricate process.

Liquidating Business setup in Dubai: Free Zone Process

Liquidating a Business setup in Dubai within a free zone (such as SPC Free Zone in Dubai) generally follows a similar logic to mainland liquidation but is managed directly by the specific free zone authority. The process is often more streamlined and can be faster than mainland liquidation.

- Shareholder Resolution:

- The shareholders or partners must pass a formal resolution to liquidate the company and appoint an approved liquidator. This resolution should be on company letterhead and submitted to the free zone authority. While notarization may not always be mandatory for free zone resolutions, it’s often preferred or required by some authorities.

- Appoint an Approved Liquidator:

- Appoint a licensed audit firm that is approved to act as a liquidator by your specific free zone authority. The liquidator will issue an acceptance letter to the free zone, confirming their role.

- Submit Initial Request to Free Zone Authority:

- Submit the shareholder resolution and the liquidator’s acceptance letter (along with a copy of the trade license, shareholders’ passports/Emirates IDs) to the free zone authority. The free zone will issue an initial approval or initiate the formal liquidation process within their system.

- Cancel All Visas and Establishment Card:

- This is a crucial early step. All active residency visas issued under the company’s sponsorship (for owners, investors, employees, and their dependents) must be cancelled. Settle all end-of-service benefits and final salaries as per UAE Labour Law.

- Once all visas are cancelled, the company’s Establishment Card (Immigration Card) must also be cancelled with the free zone’s immigration department.

- Settle All Financial Obligations and Obtain Clearances:

- Work with the liquidator to ensure all outstanding financial liabilities are settled. This includes:

- Lease Payments: Settle any outstanding rent or lease agreement obligations with the free zone and obtain a lease termination letter.

- Utility Bills: Obtain clearance from utility providers (DEWA, Etisalat/Du, etc., if applicable for your free zone setup).

- Supplier/Creditor Payments: Settle all dues with vendors and suppliers.

- Bank Accounts: Close all corporate bank accounts and obtain official bank closure letters.

- Free Zone Fees: Ensure all outstanding free zone renewal fees, penalties, or other charges are cleared.

- Federal Tax Authority (FTA): Apply for VAT deregistration (if applicable) and ensure all tax obligations (including Corporate Tax) are met and clearance is obtained.

- Customs: If it’s a trading company, obtain customs clearance.

- Work with the liquidator to ensure all outstanding financial liabilities are settled. This includes:

- Publish Liquidation Notice (if required by Free Zone):

- Some free zones may require a newspaper advertisement for a specific notice period (often shorter than mainland, e.g., 14 days or no public advertisement at all, relying on internal communication to creditors). SPC Free Zone in Dubai will advise on its specific requirements regarding public notification.

- Submit Final Liquidation Report:

- Once all clearances are obtained and liabilities settled, the appointed liquidator will prepare a Final Liquidation Report, confirming the completion of all procedures and that the company has no outstanding obligations or assets.

- Final Submission and De-registration:

- Submit the Final Liquidation Report, all original clearance certificates, and the final de-registration application to the free zone authority.

- Upon review, approval, and payment of any final de-registration fees, the free zone authority will issue a License Cancellation Certificate or a Company De-registration Letter, officially closing the Business setup in Dubai.

The timeline for free zone liquidation, including for SPC Free Zone in Dubai, is generally shorter, typically ranging from 30-60 days, assuming all documents are in order and liabilities are minimal. Professional assistance from a liquidator or business setup consultancy is highly recommended to navigate the specific free zone regulations effectively.